" 2015 must be remembered as the year of divergence. The economy “unexpectedly” fell apart in broad-based and sustained fashion, yet Janet Yellen’s pedigree still counts far more in seemingly so many places"

Jeffrey P. Snider

Alhambra Investment Partners, 31.12.2015

While we await a flood of data for December spending and retail activity to confirm what we already suspect by proxy, the updated figures for November going backwards in the production process stand as yet another warning. Retail sales figures were typically abysmal, as were private indications of spending. The Thompson Reuters Same Store Sales Index, a measure of actual dollar spending more avoiding of adjustments and imputations, posted -0.4% year-over-year “growth”; ex drugstores, the contraction was -0.7%.

The excuses for the results were long, including once more the “wrong” temperature gradient. If cold weather and residual seasonality wither the consumer in the late winter, warm weather and the lack of snow are somehow a major hindrance at its start.

"A year ago, retail sales were healthier, so beating those comparisons was tough, with 56% of retailers missing estimates. They also saw slower store traffic as online deals stole Black Friday sales. Others also blamed lower gasoline prices, foreign exchange differences, and warmer-than-usual weather."

Lower gasoline prices were supposed to be a huge, immense boost to consumer spending, while I’m not sure there would be any effect upon US consumers due to “foreign exchange differences” other than perhaps the very limited case of US retailers along the Canadian border. On the whole, Thompson Reuters now expects just 1.4% growth in the same store index for Q4 compared to 2.8% in the last three months of 2014. As always, +3% or better usually marks, for them, the dividing line between healthy and something else.

Being stranded firmly within “something else” has garnered all sorts of confusion and angst. To that end, “transitory” was meant to define “something else” as perhaps a slump but one that would not last or lead to significant alteration (without ever explaining why there might even be a temporary alteration). It was a means to express acknowledgement of the deterioration without giving it too much emphasis for fear of what that might lead to in feedback beyond the more visible economic factors.

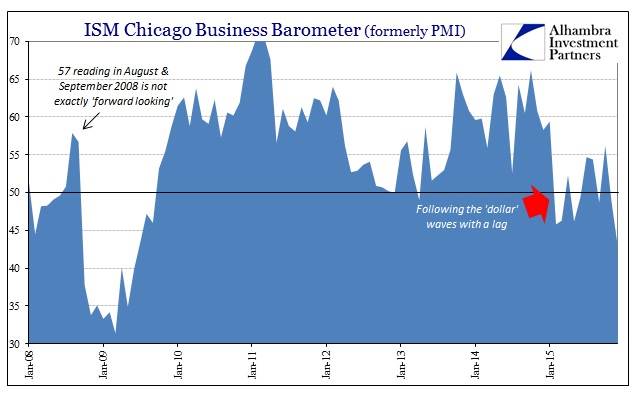

Unfortunately, the production process itself must at some point respond to these sorts of dichotomies. The idea of a manufacturing recession, as if manufacturing and goods formed some sort of economic island, is perhaps the next step beyond “transitory” in trying to isolate the “something else” as it expands. As sales continue to depress and even contract, production is indeed following (though not yet leading). The latest update to that end is the Chicago Business Barometer which dropped to just 42.9 in December, the lowest, by far, since 2009.

The decline was mostly as a result of collapsing backlogs (dropping for the eleventh straight month, from 46.6 all the way to 29.4) and new orders; in other words, businesses rapidly finishing up production from past orders and then finding no new business to replace it. Despite that, more than 55% of survey respondents expect more demand in 2016; transitory.

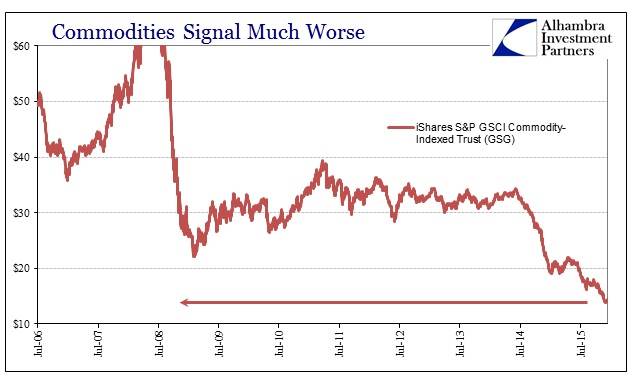

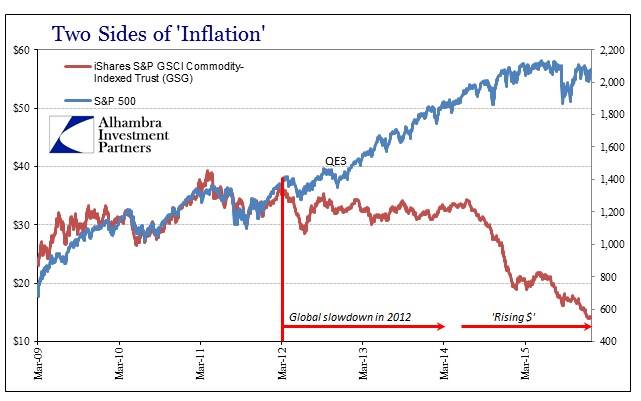

In that respect, 2015 must be remembered as the year of divergence. The economy “unexpectedly” fell apart in broad-based and sustained fashion, yet Janet Yellen’s pedigree still counts far more in seemingly so many places (apparently Chicago-area manufacturing, too). We see this in asset markets where commodity prices might sink lower and lower to new lows in a full-blown collapse, but that only generates pause and a small uptick in uncertainty and reflection. Maybe that has to do with how this “cycle” is entirely and uniquely elongated, with the economy slowing past 2012 truly confusing what might really be.

Commodity prices and stocks, for example, diverged right at that moment in 2012, with a couple QE’s wedged in there for good measure. Perhaps, in the balance of 2012, all of 2013, and the first of 2014 it was treated as the “new normal” or business as usual. Commodity prices were sideways to lower, but nothing was visibly amiss so it seemed very easy to just dismiss the growing divergence as unimportant or not meaningful. It seems as if that outlook was just as much applied even after the commodity collapse started in the middle of last year; commodities didn’t matter for years, apparently, so why pay attention now?

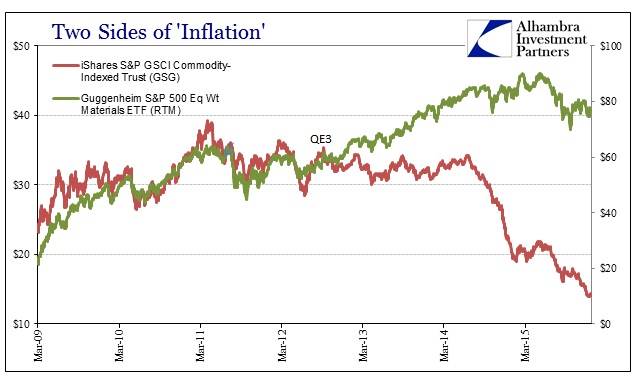

The upside down priorities contained within that sentiment were only bolstered by monetary policy, or at least perceptions and self-delusions about monetary policy (which, if it actually did what it proclaimed, would have sent commodity prices back to converge with stocks rather than gives us the current paradigm where stocks look more at risk to converge with commodities). Even in stock sectors more closely associated with commodity prices seemed unimpressed by implosion, maintaining embrace of “transitory” as if it were itself a real “thing.”

In other words, for years now “people” have been leading with the ephemeral and dismissing the real because that seemed to be the path of least resistance; to consciously set aside what is actually happening because it can only be temporary in favor of what isn’t evident now but should occur because Janet Yellen (as Ben Bernanke) says not just that it will, but that it must. The backwards placement of this kind of intuition is the only way to explain these divergences as they continue for years.

But, as noted above, convergence may already be in process though not in deference to “transitory” and the credentials of economists. As the two charts just above show plainly, commodity prices easily demonstrate no sign of stopping their trajectory while instead it has been stocks that have run into at least doubt and pause. That very much mirrors what we see in the real economy, where sales and production might still be saving for “next year’s” growth, but doubt and pause are increasingly setting “this year.” Throw in some credit irregularity, and manufacturing or industrial production doubt turns quickly to action.

It is these factors that I believe are resetting the risk spectrum for pretty much everything, economic and finance. Markets may not yet be ready to embrace commodities, but they are no longer so instantaneously flippant. Instead, the resolve of commodities and related production levels align closer and closer to credit markets, particularly junk, in order to slowly, but persistently, realign perspective and priorities back toward real conditions and away from the whispers and promises of economists and their monetary figments that play directly upon human nature. After all, recession themselves are in certain respects transitory; that’s not the actual risk.